A series of emerging trends will put pressure on modern grocery retailers to adapt. Five “resets” hold the key to continued growth.

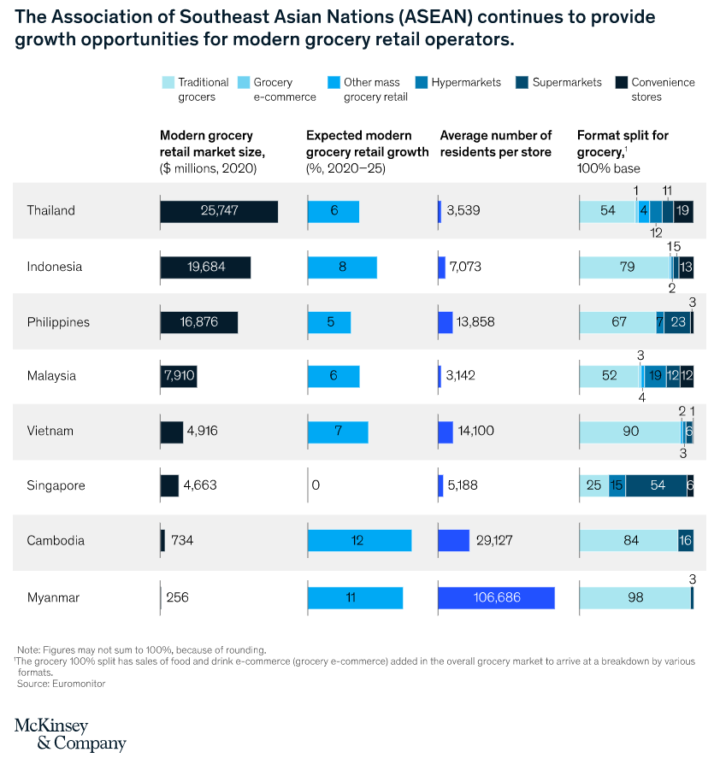

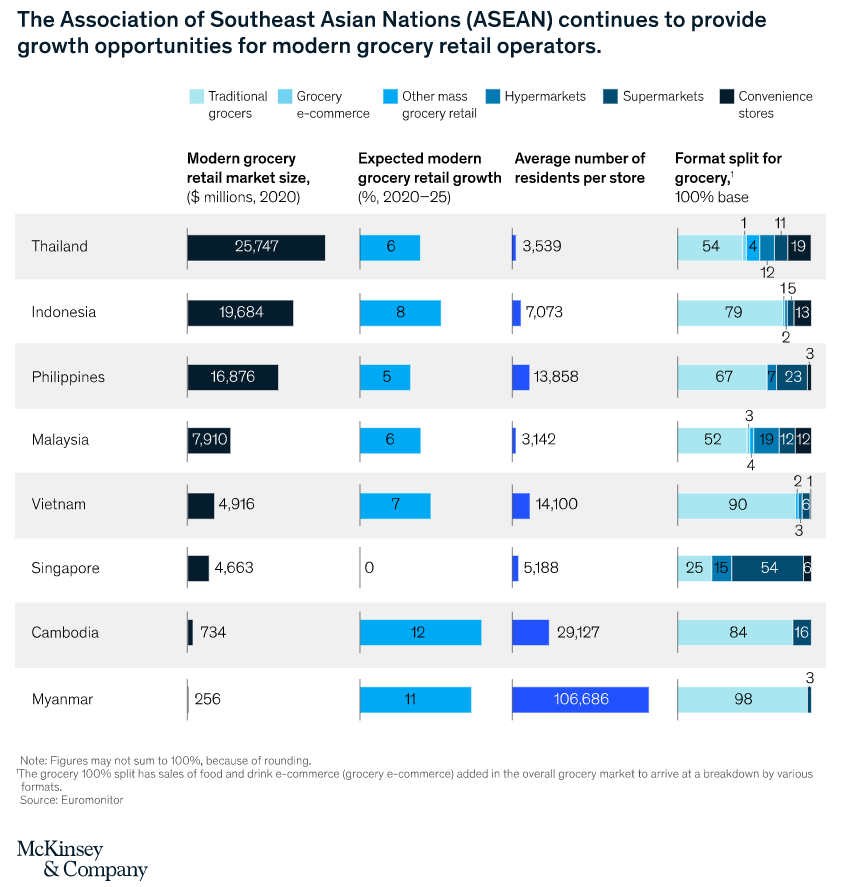

The Association of Southeast Asian Nations (ASEAN) presents potential growth opportunities for modern grocery players (Exhibit 1). The region’s more than 600 million people spend $200 billion on groceries each year, but traditional trade still accounts for two-thirds of this total—a strong indication that the modern grocery industry has headroom and the opportunity to capture a greater share of shopping needs.

Source: https://www.mas.gov.sg/news/media-releases/2023/project-nexus-prototype-links-payment-systems

Exhibit 1

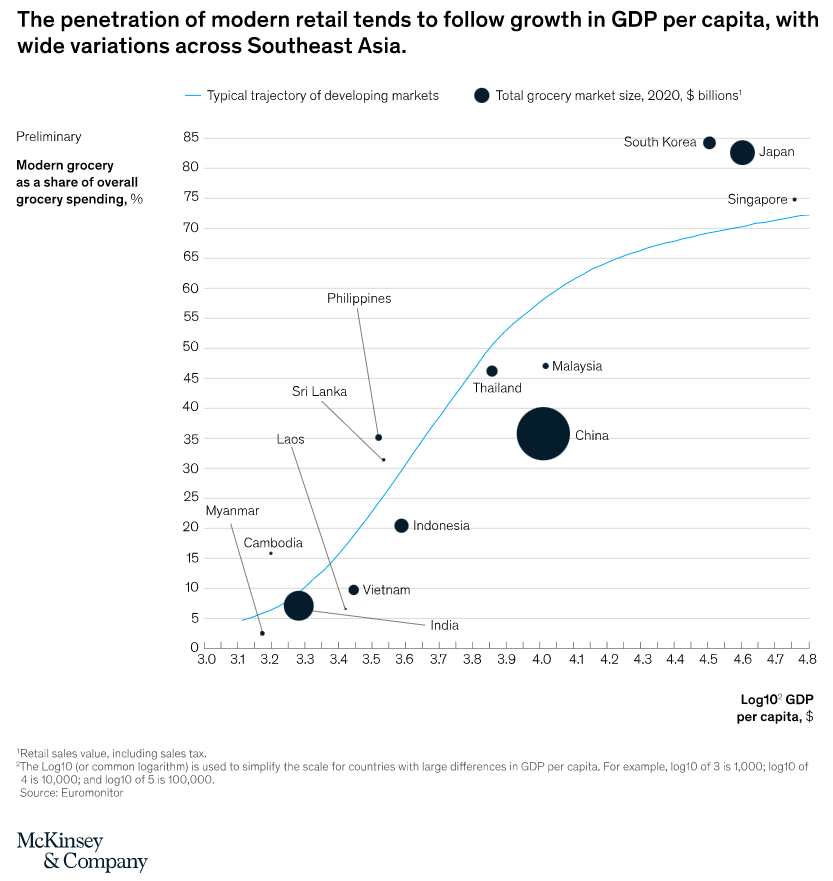

Across ASEAN, overall consumer expenditure is expected to grow about 5 percent in the next year, depending on how global macroeconomic forces affect the region. Underlying demand is higher among urban consumers, who are shifting their spending from fragmented to modern channels, creating strong tailwinds for modern retail. Our analysis projects growth of 6 to 7 percent a year for modern grocery retail through 2025, making ASEAN one of the fastest-growing and most exciting regions in the world for modern grocers (Exhibit 2).

Exhibit 2

Six emerging trends shaping modern grocery

As the industry grows, a number of developments and disruptions will intensify pressure. Modern grocery retailers must be prepared to adapt their strategy to achieve sustainable value creation and compete with fragmented trade, which itself is being reshaped by emerging eB2B platforms. We explore six trends that will influence modern grocery retail in ASEAN in the coming years:

1. Increasingly discerning consumers

The pandemic-fueled rise in grocery retail spending will likely persist even after the pandemic abates. Contributing factors include the transition to hybrid- and remote-work arrangements and the increase in dining at home.

McKinsey research has identified three distinct priorities influencing consumer purchasing decisions (see sidebar, “About the research”). Amid a period of economic volatility, consumers are tightening their belts and actively looking for ways to stretch their resources (“better value for me”). In parallel, they are working to improve their physical wellness and immunity (“healthier for me”) through healthy eating, better nutrition, and an increased focus on macro- and micronutrients. A third well-documented pattern is a willingness to purchase food online.

In the years ahead, these behaviors could become more entrenched. Consumer spending is projected to rise through 2023 and will likely be accompanied by more sophisticated purchasing behavior.

2. Fierce competition from ecosystem players

MOST POPULAR INSIGHTS

The State of Organizations 2023: Ten shifts transforming organizations

What is generative AI?

Gen what? Debunking age-based myths about worker preferences

To create lasting change, companies can draw on behavioral insights

Patagonia shows how turning a profit doesn’t have to cost the Earth

Most grocery retailers are well acquainted with increased competition from traditional players. Potentially more threatening is the rise of ecosystems and digital players with value propositions that could erode the competitive advantages of physical retailers. For example, mobility and e-commerce aggregators tend to use grocery categories to drive traffic to their own platforms.

Retailers face a vexing dilemma. By ceding core consumer interaction points to these players, they could gain a revenue source but lose out on their most precious assets: data on consumer behaviors and the ability to attract and retain consumers by creating a great experience. However, a lack of collaboration could also lead some aggregators and platforms to monetize this access (for example, with retail media networks) before retailers do.

3. A shift from growth to profitability

In many ASEAN countries, modern retail has achieved rapid growth before becoming profitable. While retailers have made remarkable headway toward profitable growth, breaking even remains a challenge, especially in online grocery, and will require new business models.

Modern grocery is expected to become prevalent in core urban areas in ASEAN over the next decade. This saturation will lead retailers to explore two new sources of growth. First, they will innovate and reorient their prepandemic customer value proposition to keep pace with new preferences. Second, they will increasingly seek to find sources of profitability, such as maintaining gross margins through negotiations, rationalizing store networks thoughtfully, or embarking on broader cost reduction initiatives.

4. Fresh offerings under pressure from digital players

Larger-format modern retailers have distinguished themselves with fresh offerings (fruits, vegetables, meat, and seafood) that are competitive on not only price but also quality and assortment. To balance quality, price, and profitability in fresh offerings, modern retailers must overcome several challenges, including securing stable, high-quality sources and maintaining consistent quality across outlets and through different seasons.

Competition is increasing: fresh produce can be purchased through e-commerce or more specialized small-scale niche supermarkets. These channels are particularly popular in countries with more mature infrastructure, such as Singapore, as well as in emerging countries like Indonesia.

5. Competing demands on omnichannel

According to our ASEAN consumer survey, e-commerce penetration in grocery, while still low, continues to grow rapidly as consumers prioritize convenience, safety, and promotions. Although consumers are embracing omnichannel, the economics remain challenging for retailers. On the one hand, the main goals for start-ups are increasing gross merchandise value and boosting user acquisition and retention. On the other hand, consumers are demanding more, and they still believe delivery charges are too expensive.

As observed in other geographies, retailers will have to refine their omnichannel positioning to strike a balance between rising consumer expectations and difficult unit economics. Options include online offers, click and collect, and partnerships with digital players.

6. A growing emphasis on sustainability

Consumers, investors, regulators, and nongovernmental organizations are pressuring companies in the food system to take tangible steps toward sustainability. Asian consumers are expressing concerns about climate change and show an increased willingness to shift their spending habits accordingly, so grocers must develop strategic sustainability transition plans. ASEAN has much catching up to do on issues such as plastic packaging, the race to net-zero emissions, and social equity. And customers, employees, and investors will increasingly hold retailers accountable for their environmental footprints.

This challenge is exceptionally complex—for instance, in the race to net zero, emissions generated from the average retailer’s own operations, together with purchased electricity and heat, are responsible for just 4 percent of the total footprint. Moreover, getting rid of plastics or making more “healthy” recipes requires consumers to fundamentally change their behavior. Retailers should view the elements of these plans primarily through the lens of value creation, since a large portion of the levers for a sustainable transition would also improve EBITDA or significantly mitigate risks.

The way forward for retailers: Five ‘resets’ for success in the next decade

Amid these significant disruptions and additional challenges, grocery retailers must move beyond focusing on factors that enable them to excel at traditional retail, such as clear value proposition, distinctive format, fresh excellence, and efficient operations. They can get started on this journey by pursuing five “resets,” which can anchor their transformation over the next decade.

Reset 1: Reframe your playing field to embrace consumer tech

Media, entertainment, food service, and food retail are increasingly converging into a “consumer tech” ecosystem, so retailers need to think like disruptors. Retailers can ask themselves the following key questions:

-

– Who is our customer?

– What is our distinctive value proposition?

– Where are our inefficiencies?

– Where can we disrupt the value chain and create a better, cheaper, more direct line to the customer?

– In which categories do we have a distinctive edge? How are we positioned in fresh? Beyond fresh, where can we offer customers the best assortment?

– How will retailers gain access to proprietary insights, assets, customers, and suppliers?

– Where can retailers partner using a programmatic mergers, acquisitions, and alliances (M&A&A) approach?

The answers to these questions can help modern retailers distill their competitive advantages and make the right investments to expand confidently beyond their existing offerings.

Reset 2: Double down on fresh, healthy, and private-label offerings before others do

Time is running out before ecosystem players, e-commerce specialists, or niche chains make major incursions into the market. To remain competitive, modern grocery players must develop compelling propositions across several categories. They can win in fresh by gaining the trust of consumers and delivering consistent quality. Augmenting the traditional product portfolio with a variety of healthy and sustainable products will enable retailers to cater to sought-after consumer segments to truly differentiate themselves in the market. Last, as consumers become more price conscious, a robust array of private-label products will help to insulate modern grocery retailers against continued inflation. These efforts require continuous improvement in sourcing and supply chain capabilities, as well as thoughtful choices on assortment.

Reset 3: Digitalize, digitalize, digitalize

Retailers no longer have excuses for not harnessing digital technologies to both elevate their consumer value proposition and improve their own operations. The only way to achieve sustained growth is to get smarter, cheaper, and faster through strategies such as serving the customer 24/7 through an online-to-offline approach, enabling precision marketing through data analytics, or using technology to automate or streamline the value chain. By incorporating data and technology, retailers can double their output and quality at half the cost. Modernizing the underlying tech stack and embracing superscaler methods will be paramount to reach consumers everywhere—and in a personalized way. In a world in which information flows freely, the winner will be the retailer with the best customer experience and the ability to scale fastest, not necessarily the biggest or cheapest retailer.

Reset 4: Pursue new revenue streams and build and scale new businesses

As the industry shifts from grocery to food retail to consumer tech, new revenue streams become available. The strongest example is retail media networks: in the wake of the shift of consumer behaviors toward e-commerce, advertising budgets are flowing toward commerce media, a new form of advertising that closes the loop between media impressions and commerce transactions to improve targeting, provide new audience insights, and deliver more relevant and valuable experiences for consumers.6 This shift is important for physical retailers, which can capture a share of this spending by developing the right offering. Other opportunities require retailers to take a “business building” lens, which could include building a private-label offering around alternative proteins or launching an e-B2B platform. In a recent McKinsey survey of executives, 52 percent of respondents indicated building new businesses was among their top three priorities.7 Retailers need to determine where they have an advantage and the time left to win and then focus on scaling faster.

Reset 5: Pursue profitable, sustainable, inclusive growth

Retailers must determine how they perform on environmental and social sustainability, where they can distinguish themselves, and what shifts are required in governance, KPIs, incentives, and work processes and culture. They will often find that near-term actions to improve sustainability can increase profitability, while broader and longer-term transformations are needed to meet expectations from shoppers, investors, and partners. To pull sustainability levers, retailers should rethink assortment, reallocate investments (including vertical integration to source more sustainably), and reinvent operations to minimize their own footprint. In practice, successful transformations need to be anchored in a transparent baseline and a portfolio of initiatives that become part of the CEO agenda.

We hope these insights inspire ASEAN grocery executives to face the future with confidence. Executives have a golden opportunity to transition their organizations from grocery retailers to players in a consumer tech ecosystem. Successful retailers will be well positioned to harness the demand from a growing middle class and shape future shopping behaviors through new experiences and new business models. These elements will ultimately be the key to crafting a path to sustainable and inclusive growth.